The Sky isn't Falling - Stop Depending on Unreliable News Sources and Antiquated Economic Barometers

With the markets slipping, during the past few weeks, from their February all-time highs, I can’t help but notice a concerted media narrative that the proverbial economic sky is falling.

I have already seen about a handful of individuals, on facebook, announce their rush to sell their assets and liquidate their retirement portfolios in preparation of the sky collapsing on their heads.

And I can sympathize with their concerns. Based on the sheer despair echoed throughout every economy-related article popping up on my newsfeed, one would think it was the year, 1933.

Having gone down the rabbit hole of America’s fiscal regulatory history, I can assure you that 2025 is the very antithesis of 1933. But I will reserve that mind-blowing discussion for a subsequent article.

In the meantime, I am going to use this piece to illustrate why I believe that today’s chicken little legacy media has it all wrong when it comes to the economy, and why investors need to stop taking agenda-driven journalism as gospel. Doing so is putting people at risk for making very unsound investment decisions that could harm their retirement plans, their children’s education and their family’s entire financial future.

Let me start by stating, emphatically, that the sky is not falling. And, even more significantly, the media is very well aware of this fact.

How could I be so sure? Well, let’s just say that when it comes to economic projections, the legacy media does not have the best track record. Well, what else would you expect when forecasts are predicated on ideology and flimsy data as opposed to objective reality?

There is no credible reason for journalists to be so pessimistic about today’s relatively small market declines when they had the complete opposite reaction, in 2022, when the markets lost more than twice as much. As of this writing, the S&P 500 is currently down 8% from its February 19th record high and NASDAQ off 12.5% from its peak.

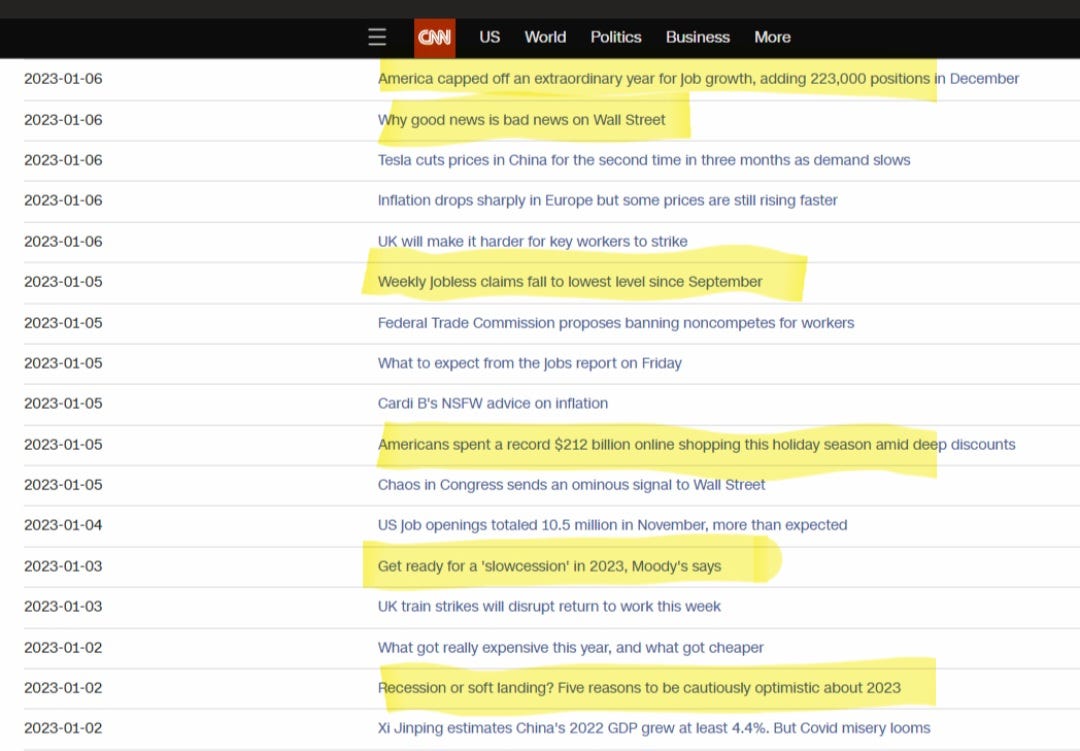

Just look at CNN’s January 2023 headlines which were fresh off the heels of the S&P 500 losing 19.6% and the Nasdaq Composite plummeting 33.5%. There was no hint of doom following the worst market performance since the 2008 global financial meltdown. Instead, CNN was encouraging its shrinking readership to be “cautiously optimistic” about the economy. The media outlet also praised the 2022 job growth as “extraordinary” (of course, this was before the employment numbers were revised downward by over 18%). CNN even went so far as to use a made-up word, “slowcession,” to avoid using the “R” word.

There were no falling sky alarms, during the previous four years, as inflation was incinerating 25% of our purchasing power; or as 401(k) hardship withdrawals surged 182% to reach new heights; or as consumer debt soared 18% to historic levels; or even as millions of more Americans slipped into poverty.1

On the contrary, tone-deaf media hacks like Paul Krugman were doing everything they could, especially during the big election year, to convince us that the economy was “Goldilocks Perfect” - even if it meant manipulating the economic data.

To paint a picture of a rosier economy, such propagandists were excluding the most inflationary and essential products as well as relying on pre-revised employment numbers to persuade the public that inflation was decelerating and that jobs were being added when, in reality, the exact opposite was transpiring.

So, after years of being fed blatant lies, forgive me for being skeptical of today’s sudden synchronized shift in negative economic sentiment - especially considering that these media “experts” are all using the same skewed data and toeing its same old agenda: to protect a 112-year-old centralized financial power structure that is in the midst of being obsoleted by decentralization.

No matter how the media attempts to spin the antiquated government data or dodgy consumer sentiment surveys, the fact is that, by definition, America is not currently in a recession. Given that the media made it vogue to use made-up terms, I am going to suggest that the nation is experiencing what I call a “purge-cession” - an economic clean-up necessary to clear the path for unprecedented prosperity.

A recession had long been defined as two consecutive quarters of negative GDP growth. Although the U.S. GDP growth slowed during the fourth quarter of 2024, it still grew 2.3%.

Since the official U.S. GDP numbers for the first two quarters of 2025 are not expected to be released until April 30th and July 30th, respectively, any talk of a present recession is pure speculation at best and fear mongering at worst.

It is worth reminding readers that, in 2022, when the U.S. actually did experience two consecutive quarters of negative GDP growth, the media reacted with the exact same feigned optimism that it held toward the 2022 tanking stock market.

In fact, here’s a link to a 2022 CNN article celebrating the second consecutive GDP contraction because it could have been lower while, at the same time, framing the long-standing “two quarter rule” as an “unofficial indicator of a recession.”

It was pretty obvious, to anyone paying attention, that CNN and other obliging media outlets received the 2022 White House talking points memo containing instructions on how to couch the indubitable RECESSION to coincide with the administration’s unilateral changes to the definition of the “R” word. The former administration strategically removed the very specific “negative two quarter GDP” standard and loosely redefined recession as a very nebulous “broad-based contraction that affects many sectors of the economy.”

If you’ve never read Ayn Rand, you may not realize the significance of replacing the objective with the subjective. This is a cute little communist tactic that gives government the power to shape a narrative as well as escape accountability.

The absence of a well-defined economic yardstick gives an obedient media the license to report based on interpretation as opposed to objective reality. This shields the government from taking responsibility for its fiscal negligence while allowing an economy to self-identify as recessionary or not.

And that, my friends, is exactly how two consecutive quarters of negative GDP growth and a 25.5% drop in the S&P 500 (from its 2022 peak to trough) does not constitute a recession; but how positive GDP growth with a 10.5% decline in S&P 500 (from its 2025 peak to trough) signifies an apparent economic apocalypse.

This brings me to my next point. Why is the S&P 500 still being viewed as a viable leading economic indicator at all?

Let’s be honest (unlike CNN), because the S&P 500 index is no longer the same diversified benchmark that once embodied the broader Main Street American economy, it has become less of an economic gauge and more of a measurement of just how dysfunctional and disproportional the U.S. public equity markets have become.

Today, just three industries (Tech, Healthcare and Financial) and seven magnificent companies (all members of the trillion-dollar market cap club) dominate the S&P 500. In fact, although they represent a mere .00002% of all American businesses, America’s seven most magnificent companies now comprise an unprecedented 35% of the S&P 500.

What’s worse is that only three investors (BlackRock, Vanguard and State Street) control the vast majority of the S&P 500 shares, collectively owning 88% of all S&P 500 companies. If that wasn’t bad enough, these hegemonic investors also just so happen to be the global leaders in passive investing - with all three utilizing quantitative investment strategies (the extent of which they refuse to disclose).

Quantitative funds, which are far more interested in a company’s trading patterns than in its goods and services, now control over 35% of the U.S. market - 44% more than funds managed by human beings, made up of flesh and blood, who possess real thoughts and emotions, and who actually buy consumer products.2

Even slight downward readjustments of the Mag Seven, by quantitative funds, are going to wreak havoc on the U.S. equity markets. This lack of “investor-base diversification” is an existential macroeconomic problem that is exacerbated by the fact that publicly traded companies, in general, are becoming a dying breed. Today, there are half as many listed companies as there were in the mid-1990s - many of which are rapidly losing all commonality with the mainstream American consumer.

In recent years, the collective revenue generated by the Mag Seven have gradually been shifting away from consumer products and gravitating towards business services. Although these services provide higher margins, this revenue repositioning is turning the S&P 500 into a better measurement of global innovation and advertising trends than a snapshot of the consumer-driven U.S. economy.

Even Amazon - a company categorized as a “Consumer Cyclical” - is increasingly generating more and more revenue from its non-consumer facing divisions like web services and advertising.

And although Telsa still serves consumers, it is, unfortunately, starting to look more like a political poll than any sort of an economic barometer.

To be clear, the S&P 500 is not the only “leading” economic indicator that is failing to accurately gauge the direction of the economy. Nearly every conventional economic metric, presently used, is either fundamentally flawed or on the cusp of being obsoleted by modern innovation - especially when it comes to the data released by the government.

Let’s start with the CPI index put out by the Bureau of Labor Statistics. Would it surprise you to learn that this consequential inflation metric, which is used to dictate life-altering fiscal policy, is months behind modern methods that use decentralized innovation to gather data?

Or would it shock you to discover that the government’s data is so deficient that it is often not even trusted by other departments within its own government? Check out my January 2023 podcast interview (especially starting at the 17:40 mark) with Stefan Rust, CEO of Truflation, an economic data provider that utilizes blockchain technology to deliver real-time, pinpoint accurate economic metrics including inflation.

What about the University of Michigan Consumer Sentiment Index, another heavily relied upon leading economic indicator? The media has been giddy concerned over its recent decline, inflaming citing inflation fears. Given the media’s reputation for deceit, it begs questioning whether or not consumer sentiment is indeed deteriorating and whether or not inflation is factually on the rise.

Truflation, which again is months ahead of the government figures, shows true inflation to be down over 17% from a month ago and 40% lower than it was a year ago.

As far as consumer sentiment is concerned, according to Truflation CEO Stefan Rust, “There is a big difference between what people say and how they think and feel.”

That was a lesson that pollsters learned all too well in 2016.

Fortunately, everyone will soon learn exactly how consumers are feeling as word on the blockchain street has it that Truflation will be launching its own consumer sentiment index - one based precisely on a consumer’s state of mind.

Before you allow tales of a falling sky push you into investing hibernation, it would behoove you to explore these more sophisticated, real-time economic data tools. This may just be what saves you from waking up to find that the only thing that fell was your net worth.

This article is for informational purposes only and is not intended to be personal financial advice. Please obtain independent financial advice before making any investment decision based on the information contained on this website.

Sources: Federal Reserve, US Census, Vanguard

The Economist